Polity: House-buying patterns in Auckland

506 Responses

First ←Older Page 1 … 10 11 12 13 14 … 21 Newer→ Last

-

BenWilson, in reply to

The RBNZ stress tests last year showed the banks could withstand a 50% fall in house prices and unemployment reaching double digits.

LOL. Yup. Right. A sudden 50% drop in the value of their entire asset base would just be laughed off and all the unemployed and also now homeless would be fine cause social welfare.

-

going back to when I was looking into this in 2013, here is another document, where I was using other numbers that gave similar conclusions, but it is much harder to follow the argument as it is more mathematical.

https://www.dropbox.com/s/tlkq1efejjk0lhv/housepricesanalysis.pdf?dl=0

-

Stephen Judd, in reply to

A sudden 50% drop in the value of their entire asset base would just be laughed off

But a 50% drop in house prices is not a 50% drop in banks' asset bases; their asset base is the total outstanding loans secured against those houses. And NZ doesn't let you just walk away if you're underwater, unlike some US states, so those loans won't be impaired that badly.

-

BenWilson, in reply to

Yeah. Or even simpler, just make the cost of housing part of the basket of goods in the inflation calculation. Not that unreasonable, since everyone except the actual homeless have to finance a roof over their heads somehow. The idea of inflation is meant to be around "the rising cost of living" or "the declining value of money", which is much the same thing. It's meant to be a measure of "what your money can buy". If one of the three basics of life (food, shelter and water) has skyrocketed in cost, then it's hardly unfair to count it in the inflation statistics. I can do without a fancy TV, but a roof? Not so much.

-

Katharine Moody, in reply to

Very interesting - thanks!

-

BenWilson, in reply to

But a 50% drop in house prices is not a 50% drop in banks’ asset bases; their asset base is the total outstanding loans secured against those houses.

That’s true enough. In my case, with about 50% equity, I’d just lose everything, and the bank would lose nothing except for my ongoing mortgage repayments. So yes, you’re right, they would not lose 50% of their wealth. But the nation collectively would lose pretty near that. The banks might survive that…depending what you mean by surviving. It’s pretty hard to imagine that scenario NOT leading to a full scale reevaluation of the entire finance sector’s role in the economy.

ETA: I mean, I'm trying to imagine the nation laughing off a scenario wherein every single homeowner with less than 50% equity is suddenly effectively insolvent. Basically every young family that has a property in NZ is suddenly worth negative hundreds of thousands of dollars. That's not going to stress the nation one little bit, right?

-

Rich of Observationz, in reply to

The answer would be a scheme where the state bails out the (former) home-owner by swapping their unpayable debt for government bonds, taking ownership of the property and granting them a lifetime, maintaining tenancy. Then put the properties into community co-operatives so that people have collective control over "their" joint properties rather than dealing with the government directly.

Dancing Cossacks FTW!

-

Swan, in reply to

"However, reflecting strong underlying earnings in the

New Zealand banking system, these factors were only

sufficient to cause negative profitability in a single year

in each scenario"http://www.rbnz.govt.nz/financial_stability/financial_stability_report/fsr_nov14_boxa.pdf

-

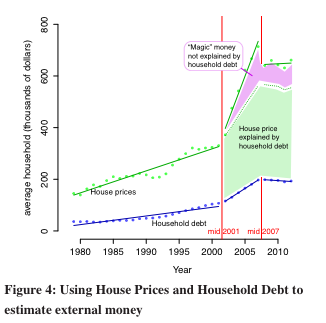

And another graph from around the time- keeping in mind that this is showing 1980-2012 (rather than the early 2000s bubble period of the graph a few pages ago) and being generous with the assumptions about how much could be explained with household debt.

In the accompanying text I wrote, in mid 2013, "And now the worrying bit. The period after 2007 actually fits better if it has the same slope as pre 2002 then has a sudden increase in 2012 (the early 2013 data also supports this). This suggests we may be entering a period of further off-shore money coming in, further pricing out New Zealand households"

-

David Hood, in reply to

Basically every young family that has a property in NZ is suddenly worth negative hundreds of thousands of dollars.

It basically means you a never ever moving, so not likely to be ever changing jobs etc.

-

Katharine Moody, in reply to

Really useful analysis. I wonder if another data set to be considered as a predictor might be migration and immigration. Steven Joyce (and perhaps John Key as well) had been running the line that on the demand side, the problem was fewer NZers heading to Aus and more coming home. Used to counter the argument that it was non-resident purchases driving the price hikes.

-

Alfie, in reply to

Basically every young family that has a property in NZ is suddenly worth negative hundreds of thousands of dollars.

Keep in mind Ben that the housing bubble is pretty much confined to Auckland. When (not if) that bubble bursts, the damage will most likely be confined to Akl. The housing market in the South Island -- except in ChCh, cos earthquakes -- is relatively stable and tends not to suffer the up/down cycles of more volatile markets.

We're a staunch lot down here.

-

Swan,

"ETA: I mean, I’m trying to imagine the nation laughing off a scenario wherein every single homeowner with less than 50% equity is suddenly effectively insolvent. Basically every young family that has a property in NZ is suddenly worth negative hundreds of thousands of dollars. That’s not going to stress the nation one little bit, right?"

For any household who owns only their own home (or a single home they dont live in that approximates their living requirements), they are effectively "neutral" when it comes to the housing market.

A household who does not own a house at all is "short" on housing. They consume one house worth of housing and so are negatively effected when the price of housing rises, and benefits when it falls.

A household that owns multiple house is "long" on housing. They consume one house but have more than one. So they are positively effected when the price of housing rises, and similarly negatively affected when it falls.

For a household with one house, they are not significantly affected. Sure their net worth on paper drops, but their mortgage costs are unchanged and they still own and have a house to live in.

So basically, its a wash and as long as the financial system comes through OK the RBNZ should be able to stabilise employment etc (if they are competent.

-

A C Young, in reply to

"Or even simpler, just make the cost of housing part of the basket of goods in the inflation calculation"

Actually I believe that it is:

http://www.stats.govt.nz/tools_and_services/newsletters/price-index-news/Apr%20-14/purchase-of-housing-and-rentals-in-the-cpi.aspxAccording to that page, building a new house or renting an existing one are both part of the basket.

What is not part of the basket is the cost of the land itself.

-

David Hood, in reply to

When I looked at it (so up to 2012) I found that immigration was not actually a very good prediction of house prices compared to the arrival of money, and the two did not have very much of a relationship between them.

-

David Hood, in reply to

The CPI basket tracks rentals and new houses only- not sales of existing houses. Think of it as the construction materials.

-

Katharine Moody, in reply to

When I looked at it (so up to 2012) I found that immigration was not actually a very good prediction of house prices compared to the arrival of money, and the two did not have very much of a relationship between them.

Well, that's very interesting as well.

-

BenWilson, in reply to

So basically, its a wash and as long as the financial system comes through OK the RBNZ should be able to stabilise employment etc (if they are competent.

They'd have their work cut out for them. Show me a country that's actually had this happen and I might believe it. Calling it a wash that huge numbers of people lose more than everything they have is a pretty simplistic. What could the RBNZ do about it? Presumably you mean some real emergency measures, like what the US Reserve Bank did when faced with a smaller collapse?

Bear in mind that a property collapse isn't just going to be this isolated event. There are a great many things that rely on the value of property, and cascading collapses of all kinds can happen at the same time. Any business with high leverage is going to be severely affected by debt drying up. The construction industry is pretty much going to immediately stall, putting tens of thousands out of work. Small businesses secured against property might well be completely screwed. A whole lot of farms are going to be appraised as insolvent. The banking sector itself will shed jobs massively. Lots of leveraged property investors will be bankrupt. The dollar would probably collapse, killing importers, driving up prices of all imported goods. All NZers with any assets here would have become rapidly objectively a lot poorer. Only for people with no assets at all would it be a wash, and then only if they kept their jobs. But they're the least likely people to keep their jobs, because it's generally the poorest people who have the most tenuous employment in the first place.

-

nzlemming, in reply to

A whole lot of farms are going to be appraised as insolvent.

This is (quietly) happening already. Our over reliance on dairy has caused many farmers to go so far into debt they will never get out unless the milk price magically rebounds to peak levels and stays there. Not going to happen.

-

I have to say that it's pretty amusing that in economics, "stress testing" doesn't involve actually putting anything under stress. Their "stress testing" is modelling the scenario with a spreadsheet. If only I could do that for software I wrote, I'd pass every stress test ever. Of course it would fall over in practice.

-

Sacha, in reply to

Attributing the problem to consents and zoning is pretty much an unsupported assertion.

Also a convenient right-wing talking point. Look guv, it's all the council's fault.

-

BenWilson, in reply to

The annoying thing is that it probably does have seeds of truth. Rising compliance difficulties probably are one of the contributing factors to rising costs. The question is about how much of a factor they are. And we can't know that without a semi complete picture of the drivers to even do modeling around.

-

Sacha, in reply to

Opposition parties have agreed to change those parts of the RMA that are pointlessly slowing down what councils can do. There was also a big over-correction in appetite for risk after the cost of leaky buildings landed on councils rather than govt or cowboy builders and developers.

-

Sacha, in reply to

The question is about how much of a factor they are.

you might find this Transportblog post interesting.

-

Rich of Observationz, in reply to

It's only the land that has long term value and inflates. The shack you built on it will be firewood in a few hundred years, and the flash kitchen will be in the dump shop in thirty. People forget this as part of their house porn fueled delusions, of course.

Post your response…

This topic is closed.